A2A Transactions

TodayPayments.com is a leading U.S. fintech

platform for automating A2A transactions via open banking, ISO 20022

messaging, and real-time payment networks like FedNow®, RTP®, and

Same-Day ACH.

We offer merchants, vendors, and finance

teams a digital-first solution for invoicing, alias-based payments, and

secure HTML payment page delivery — with guaranteed “Good Funds” every

time.

A2A Transactions A2A Transactions Enhanced by Open Banking and Real-Time Payment Networks

![]() As payment expectations evolve, businesses must

move beyond outdated ACH systems and manual billing cycles. That’s

where A2A (Account-to-Account) transactions come in —

enabling fast, verified payments between payer and payee using open

banking infrastructure and real-time rails like FedNow®, RTP®,

and Same-Day ACH.

As payment expectations evolve, businesses must

move beyond outdated ACH systems and manual billing cycles. That’s

where A2A (Account-to-Account) transactions come in —

enabling fast, verified payments between payer and payee using open

banking infrastructure and real-time rails like FedNow®, RTP®,

and Same-Day ACH.

With TodayPayments.com, you can request and receive A2A payments instantly, embed secure HTML links into invoices, verify payer identity via Confirmation of Payee, and automate reconciliation with ISO 20022-compliant messaging all from a single platform.

Account-to-account (A2A) payments allow businesses to move money instantly and directly between bank accounts. Whether you're managing B2B supplier payments, C2B subscriptions, or internal A2A transfers, open banking combined with FedNow®, RTP®, and Same-Day ACH makes it possible to request and settle payments in seconds with confidence.

Key Capabilities:

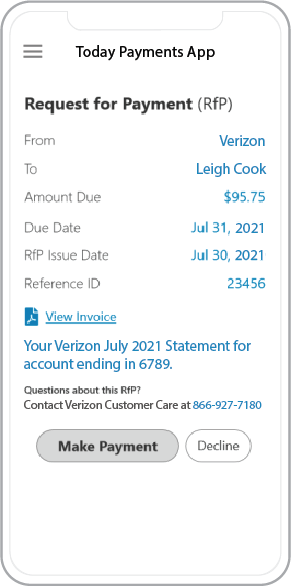

- Use .html payment links embedded in digital invoices

- Accept payments via Same-Day ACH, RTP®, FedNow®, or credit card fallback

- Support one-time, recurring, static, or variable billing

- Automate alias-based payments using mobile number or email address

- Guarantee real-time delivery with “Good Funds” settlement

- Enable push or pull transaction logic for full flexibility

Batch Uploads + ISO 20022 Messaging = Smarter, Scalable Payment Requests

No matter your payment volume, TodayPayments.com supports structured batch file uploads in ISO 20022 format to streamline invoicing and settlement across all institutions — from local credit unions to national banks.

Supported File Formats:

- ✅ .Excel, .XML, and .JSON for seamless system integration

- ✅ Real-time Request for Payments (RfP) with alias mapping

- ✅ Identity verification through Confirmation of Payee

- ✅ Payment routing through FedNow® and RTP® networks

- ✅ Email, SMS, or text invoicing with clickable hosted links

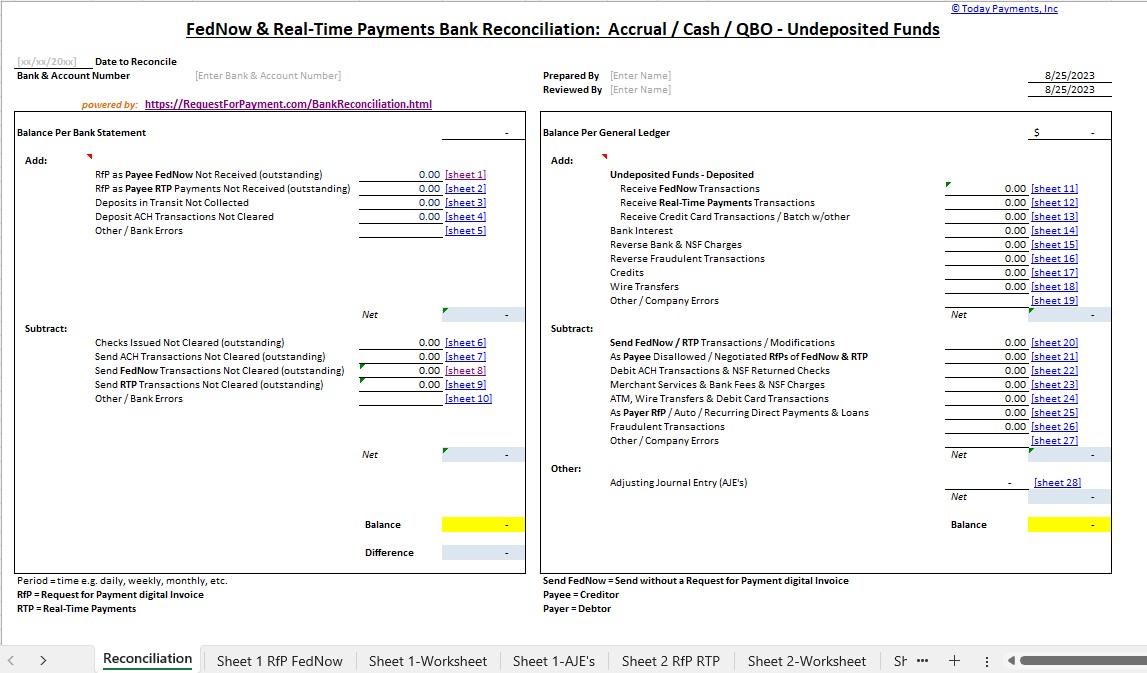

- ✅ Smart reconciliation with free A2A Bank Reconciliation templates

From small businesses to enterprise-scale operations, we give you tools that grow with your billing complexity.

From Alias to Instant Payment: Real-Time A2A Invoicing in Action

The power of A2A lies in simplicity and certainty. With TodayPayments.com, you can skip the slow ACH wait and use real-time networks to accept payments 24/7, fully verified and auto-matched to your accounting system.

What Sets Us Apart:

- ✅ Alias-based invoicing — no sensitive account data required

- ✅ Hosted payment pages via email, text, or app

- ✅ ISO 20022-rich data messaging for smart transaction handling

- ✅ Support for recurring billing and one-off invoices

- ✅ Instant confirmation of “Good Funds” with FedNow® or RTP®

- ✅ 24/7 online enrollment — no bank visits needed

- ✅ Free Reconciliation Worksheets to streamline cash tracking

✅ "FREE" Real-Time Payments Bank Reconciliation – with all merchants process with us.

Business merchants using FedNow can greatly benefit from adopting Account-to-Account (A2A) transfers for receiving and making payments. These transfers, enabled through open banking, address key industry concerns like security and transparency, while offering the potential to drive the adoption of real-time payments via systems like FedNow, Real-Time Payments (RTP), and ACH. Here's why FedNow business merchants should use A2A transfers:

1. Real-Time Payment Settlement

- Instant Access to Funds: A2A transfers allow merchants to receive payments instantly through FedNow. Unlike traditional payment methods that take 1-3 business days for settlement (e.g., ACH or card payments), FedNow enables businesses to access their funds in real time, ensuring immediate liquidity.

- Improved Cash Flow: For merchants, having immediate access to funds is critical for managing working capital, paying vendors, or reinvesting in their business. With A2A transfers, businesses can speed up their cash flow cycles.

2. Lower Transaction Costs

- Avoid Credit Card Fees: One of the significant advantages of A2A transfers is that they bypass expensive credit card interchange fees and other processing fees. FedNow A2A transfers go directly from the customer's account to the merchant’s account, which reduces the overall cost of transactions.

- Eliminating Middlemen: A2A payments remove the need for intermediaries (such as card networks) that typically take a cut of each transaction. This direct connection saves costs, particularly for businesses handling high volumes of transactions.

3. Enhanced Security

- Secure Open Banking Framework: A2A payments benefit from the secure data-sharing environment enabled by open banking. With strong encryption and secure APIs, sensitive financial data is protected, minimizing the risk of fraud or data breaches.

- Fraud Prevention: Since A2A transactions are initiated directly from the payer’s bank account, they are subject to higher levels of authentication (such as multi-factor authentication or biometric verification), significantly reducing fraud risk. For merchants, this means fewer unauthorized transactions and chargebacks.

4. Frictionless Customer Experience

- Simple and Fast Payment Process: Customers can authorize A2A payments directly from their bank accounts, providing a smooth and simple payment experience. By removing the need for card details or third-party payment gateways, the checkout process is faster, improving the overall customer experience.

- Instant Payment Confirmation: Customers and merchants receive real-time confirmation of transactions, which fosters trust and reduces payment-related disputes. Merchants can immediately confirm payment receipt and provide faster services or product fulfillment.

5. Reduced Chargebacks

- Irreversible Payments: Unlike credit card payments, which can lead to chargebacks, A2A payments are generally final and irreversible once authorized by the customer. This reduces the financial and administrative burden on merchants caused by chargeback disputes, providing more certainty with each transaction.

- Lower Risk of Disputes: Since customers authorize A2A payments through their bank accounts, they have more control over the transaction, reducing the likelihood of disputes or payment reversals.

6. Transparency and Control

- Real-Time Payment Tracking: A2A transfers through FedNow give merchants full visibility into the payment process. With real-time tracking, businesses can see the status of transactions and manage payments efficiently, improving their financial management and operations.

- Easier Reconciliation: The immediate confirmation of payments simplifies the reconciliation process, allowing merchants to match incoming payments with invoices or orders quickly. This reduces errors and streamlines bookkeeping efforts.

7. Compliance and Data Privacy

- Regulatory Adherence: FedNow operates within the framework of open banking, ensuring that merchants comply with strict regulatory standards around data security and privacy. Open banking mandates transparency and requires strong customer authentication, helping merchants meet compliance requirements while safeguarding customer data.

- Data Privacy for Customers: Customers feel more secure knowing their financial data is being shared in a controlled and regulated environment. By using secure APIs for A2A transfers, merchants can reassure customers that their data is handled safely.

8. Real-Time Payments (RTP) and ACH Compatibility

- FedNow and RTP Integration: A2A payments support real-time payment rails such as FedNow and RTP, ensuring that businesses can take full advantage of instant transactions. Merchants can accept payments faster, which speeds up order fulfillment and service delivery, enhancing customer satisfaction.

- ACH for Lower-Cost Payments: While FedNow offers real-time transactions, A2A transfers can also work with ACH payments, which are typically lower-cost. This allows merchants to choose the payment speed and method that best suits their needs, providing flexibility for businesses with different payment requirements.

9. Better Financial Planning and Flexibility

- Improved Liquidity Management: With the ability to receive payments in real time, merchants can better manage their cash flow and adjust to changes in business operations more quickly. Instant A2A transfers enable businesses to react swiftly to market demands, making them more agile and financially prepared.

- Simplified Payroll and Vendor Payments: Merchants can also use A2A transfers for making payments, such as payroll and vendor payments. With real-time settlements, businesses can ensure timely payments to employees and suppliers, improving business relationships and operational efficiency.

10. Cost Savings on Cross-Border Payments

- Reduced Cross-Border Fees: A2A transfers through FedNow and other real-time payment systems can be more cost-effective for cross-border transactions compared to traditional wire transfers or card payments, which carry high fees. This is particularly beneficial for businesses that engage in international trade or deal with overseas suppliers.

- Faster Cross-Border Settlements: Instead of waiting days for cross-border payments to clear through conventional channels, merchants using A2A transfers can receive payments more quickly, reducing delays and ensuring faster delivery of goods and services.

11. Adaptability to Future Payment Innovations

- Scalability: As the financial landscape evolves, A2A payments via FedNow provide a scalable payment infrastructure that can grow with a business. Whether a merchant handles a small number of transactions or a high volume of real-time payments, the system can adapt to business needs.

- Future-Proofing Payments: By adopting A2A transfers and integrating them with FedNow, merchants are positioning themselves to take advantage of future developments in payment technologies. Real-time, secure, and direct payment methods will likely become the standard, and businesses that adopt them early will stay ahead of the competition.

Conclusion

FedNow business merchants should adopt A2A transfers because they offer significant advantages in terms of real-time payment settlement, lower transaction costs, enhanced security, and an improved customer experience. By addressing industry concerns and providing a secure, regulated environment for data sharing, open banking ensures that A2A payments can reach their full potential, driving forward the adoption of real-time payments via FedNow, RTP, and ACH. For merchants, this means faster payments, better cash flow management, reduced costs, and an overall more efficient and secure payment process.

Request. Receive. Reconcile — in Real Time.

Still waiting on checks? Struggling with ACH

delays?

TodayPayments.com gives your business the tools to

send payment requests and get paid instantly via FedNow®, RTP®, or ACH

— all verified, all secure, and all automated.

✅ Alias invoicing with email or

phone

✅ One-click payment via link (HTML payment page)

✅ Batch uploads with ISO 20022 compliance

✅

Free reconciliation templates for your team

✅ Instant

crediting with “Good Funds” guarantee

👉 Start processing A2A transactions the modern way at TodayPayments.com — where your payments are fast, verified, and real-time.

Creation Request for Payment Bank File

Call us, the .csv and or .xml FedNow or Request for Payment (RfP) file you need while on your 1st phone call! We guarantee our reports work to your Bank and Credit Union. We were years ahead of competitors recognizing the benefits of RequestForPayment.com. We are not a Bank. Our function as a role as an "Accounting System" in Open Banking with Real-Time Payments to work with Billers to create the Request for Payment to upload the Biller's Bank online platform. U.S. Companies need help to learn the RfP message delivering their bank. Today Payments' ISO 20022 Payment Initiation (PAIN .013) shows how to implement Create Real-Time Payments Request for Payment File up front delivering a message from the Creditor (Payee) to it's bank. Most banks (FIs) will deliver the message Import and Batch files for their company depositors for both FedNow and Real-Time Payments (RtP). Once uploaded correctly, the Creditor's (Payee's) bank continues through a "Payment Hub", will be the RtP Hub will be The Clearing House, with messaging to the Debtor's (Payer's) bank.

Call us, the .csv and or .xml FedNow or Request for Payment (RfP) file you need while on your 1st phone call! We guarantee our reports work to your Bank and Credit Union. We were years ahead of competitors recognizing the benefits of RequestForPayment.com. We are not a Bank. Our function as a role as an "Accounting System" in Open Banking with Real-Time Payments to work with Billers to create the Request for Payment to upload the Biller's Bank online platform. U.S. Companies need help to learn the RfP message delivering their bank. Today Payments' ISO 20022 Payment Initiation (PAIN .013) shows how to implement Create Real-Time Payments Request for Payment File up front delivering a message from the Creditor (Payee) to it's bank. Most banks (FIs) will deliver the message Import and Batch files for their company depositors for both FedNow and Real-Time Payments (RtP). Once uploaded correctly, the Creditor's (Payee's) bank continues through a "Payment Hub", will be the RtP Hub will be The Clearing House, with messaging to the Debtor's (Payer's) bank.

... easily create Real-Time Payments RfP files. No risk. Test with your bank and delete "test" files before APPROVAL on your Bank's Online Payments Platform.

Today Payments is a leader in the evolution of immediate payments. We were years ahead of competitors recognizing the benefits of Same-Day ACH

and Real-Time Payments funding. Our business clients receive faster

availability of funds on deposited items and instant notification of

items presented for deposit all based on real-time activity.

Dedicated to providing superior customer service and

industry-leading technology.

1) Free ISO 20022 Request for Payment File Formats, for FedNow and Real-Time Payments (The Clearing House) .pdf for you manually create "Mandatory" (Mandatory .csv or .xml data for completed ISO 20022 file) fields, start at page 4, with "yellow" highlighting. $0.0 + No Support

2) We create .csv or .xml formatting using your Bank or Credit Union. Using your invoice information database to create an existing Accounts Receivable file, we CLEAN, FORMAT to FEDNOW or Real-Time Payments into CSV or XML. Create Multiple Templates. You can upload or "key data" into our software for File Creation of "Mandatory" general file. Use either the Routing Number and Account Number for your Customers or use "Alias" name via Mobile Cell Phone and / or Email address.

Fees = $57 monthly, including Activation, Support Fees and Batch Fee, Monthly Fee, User Fee. We add your URI for each separate Payer transaction for additional Payment Methods on "Hosted Payment Page" (Request for file with an HTML link per transaction to "Hosted Payment Page" with ancillary payment methods of FedNow, RTP, ACH, Cards and many more!) + $.03 per Transaction + 1% percentage on gross dollar file,

3) Add integrating QuickBooks Online "QBO" using FedNow Real-time Payment using our A2A Transactions system.

Fees Above 2) plus $29 monthly additional QuickBooks Online "QBO" formatting, and "Hosted Payment Page" and WYSIWYG

4) Above 3) plus Create "Total" (over 600 Mandatory, Conditional & Optional fields of all ISO 20022 Pain .013) Price on quote.

Each day, thousands of businesses around the country are turning their transactions into profit with real-time payment solutions like ours.

Contact Us for Request For Payment payment processing